Have you ever felt anxious when trying a new dish (especially for guests?) You fret whether it will turn out right. Not just is the success of the celebration on the line, maybe your reputation in the kitchen is too. Retirement preparation and investing can evoke a comparable sense of anxiety, though naturally the stakes are much higher. In both cases, we have a keen interest in the result, matched with a sense of unpredictability about what that result might be. As someone who has actually spent decades doing both professionally - cooking and providing retirement/investment assistance - I provide some tips from the kitchen area that can be used to successful planning for the future.

This looks like an obvious observation, however the majority of young specialists do not have budgets set out, and do not even know their present wages. It is a good concept to keep a running list of costs, including monthly and high-end, to comprehend needs and lost cash.

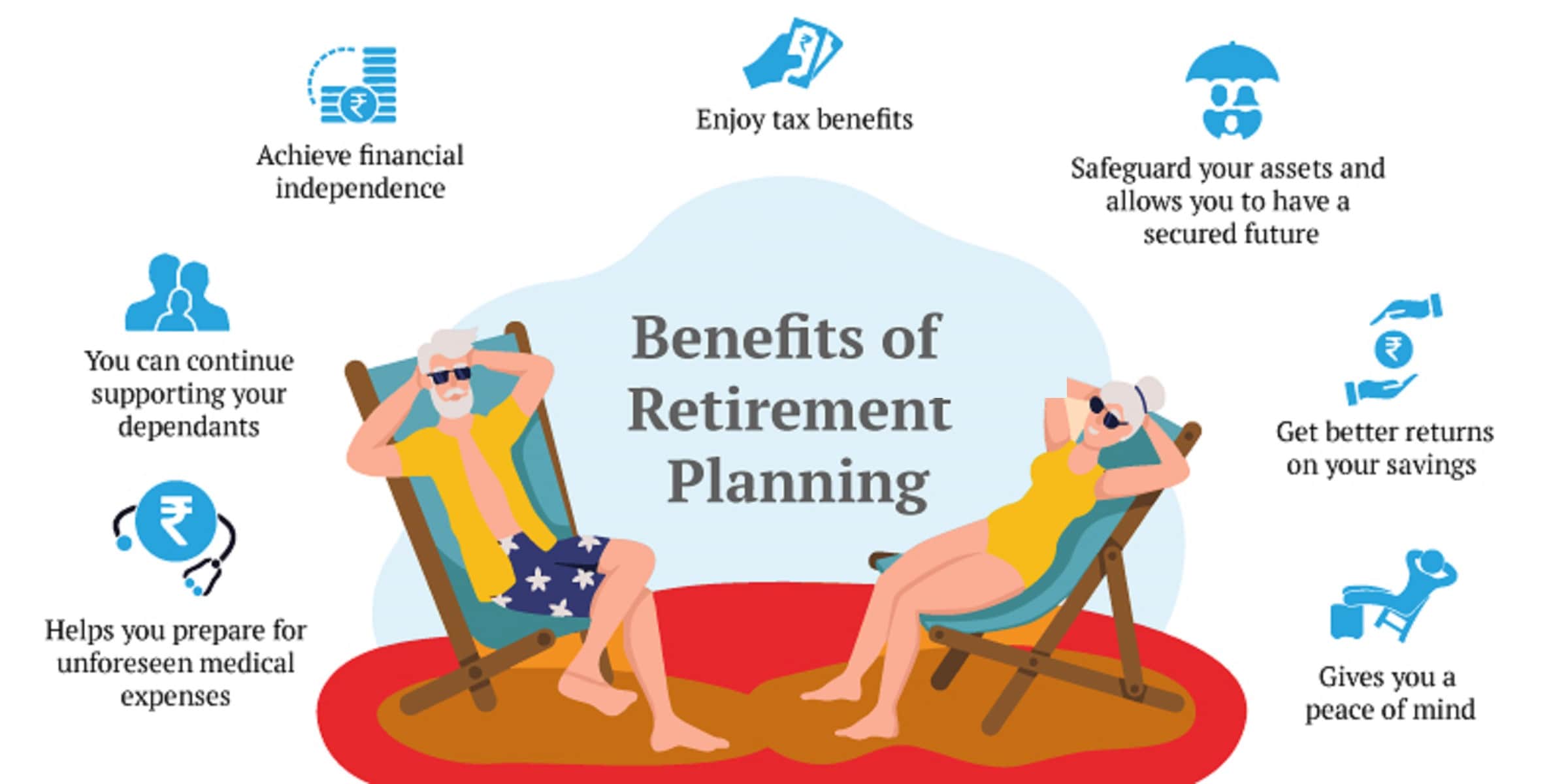

The typical point is money looses its value over a duration of time. A rupee worth tomorrow will be lower than rupee worth today, courtesy monster called inflation. So inflation ends up being the single essential aspect to prepare for retirement.

Absolutely nothing is chillier and lonelier than aging. Being economically self sufficient can give a great deal of warmth in all aspects, psychological, social and familial. There is honey if there is money. There is a statistics about retirement planning. To delight in a minimum of half the high-ends that you delight in today, you need to save at least quarter of your earnings for the retirement. This is considering today rate of inflation. Yes it is a bit idealistic. However if we could conserve half of what is ideal it would offer us a company assisting hand.

Required necessary retirement ages do not work. The option is either to extend your career or have a second career. retirement planning Due to the unpredictability of the future, living longer and low financial investment returns the majority of people will have to work longer. For many individuals this may be a preferred choice as apart from the health and durability benefits what will one finish with great deals of time however no cash?

At this moment you will also want to choose when you are going to retire. This is essential when it comes to choosing the dollar amount you will require. Your 2nd step is to get an excellent financial planner who will be able to help you come up with an excellent strategy that will work for you, and prepare you for retirement.

The basic retirement age is 65, while many get social security advantages starting at 62. Nevertheless, we are starting to see lots of people developing into their seventies and eighties, retiring much later than they did previously. You will require to make a great price quote of when you believe you will retire, but 65 is probably a safe guess.

This is the most helpful aspect of the financial investment. The disadvantage of the plan is that there is a lock in duration. You may not have the ability to utilize the cash when you require it might be more than at the old age.